Unlocking Stablecoins’ Full Potential for the Masses

What past innovation cycles reveal is needed for mass adoption of stablecoins.

A dollar is supposed to be a dollar—but why doesn't it always feel that way? Multi-day settlement times, fragmented payment systems, and high transaction fees often reveal the inefficiencies that weaken its value in practice.

Since the earliest forms of currency, people have sought to address problems with value transfer. Stability, accounting, and efficiency are ways currencies and subsequent infrastructure improvements have tried to solve these problems. After many iterations of currency as we know it today, it wasn’t until a little over a decade ago that people began to address the challenges surrounding trust, starting with blockchain systems.

Blockchain removed the need for counterparty trust in a system—the advent of smart contracts allowed for onchain ‘crypto’ assets to be programmable. Stablecoins were one of many types of assets that started to come onchain.

In 2014, the first stablecoin, BitUSD, was launched, kickstarting a rapid race of stablecoin innovation. Each new stablecoin, Tether (USDT), USD Coin (USDC), Dai (DAI), and many others, promised variations of a familiar government-backed currency but were more efficient and open in their designs. Compared to legacy solutions that don't use blockchain, nearly all stablecoins promise lower transaction fees and faster settlement. People have recognized these benefits, and increasingly so over time. Since October 2019, the stablecoin market has grown from a total circulating supply of $2.8 billion to $189.2 billion, a 5,693% increase![1]

Although stablecoins successfully address many longstanding issues in monetary systems and payment systems, their current market represents just a fraction of the global financial ecosystem. With the world's GDP exceeding $100 trillion, stablecoins have enormous room for growth. Trends in past financial innovation cycles suggest that new financial asset growth begins with a clear use case, but mass adoption hinges on innovations streamlining infrastructure.

The Advent of Currencies Solving Fundamental Problems

Bartering, the earliest form of trade, had significant and obvious flaws: it was inefficient, lacked a standard measure of value, and goods often depreciated over time.

The inefficiencies of bartering led to the creation of the first minted coins (many believe by the Lydians in the 7th century BCE), a solution that transformed trade by providing stability and a universal standard of value. Markets could now be more unified, and people could more easily preserve their wealth.

Currencies continued to evolve to address similar problems centuries later but at scale. Even in the United States there was a highly fragmented currency system used by the American colonies; foreign currencies, currencies issued by different colonies, and barter were common means of exchange.

Later in the 20th century, the Chinese faced similar issues, with a recent civil war splitting the country into smaller regions, many of which issued their own currencies. Some even adopted Japan’s currency after its invasion during the Second Sino-Japanese War (1937-1945). To simplify their economies, the U.S. and China introduced today’s dollar and renminbi to address fragmentation and asset volatility within their countries.

Sovereign Currencies’ Rapid Acceleration During the Digital Age

The launch of interbank communication systems and the subsequent growth of the internet marked an inflection point in financial technology, greatly enhancing the usefulness of both sovereign currencies by making them more accessible and practical for global and local transactions. In the 20th century, systems like SWIFT (1973) and later CIPS (2015) revolutionized cross-border payments, standardizing communication and reducing inefficiencies in global financial transactions.

In the 2000s, digital banking began rapidly adopting Internet technologies in the U.S. By this time, most American banks were offering online banking services, and their applicable use cases extended even further, with new tech giants like PayPal, Amazon, and Google increasing the usage of the dollar.

The U.S. upgraded its financial infrastructure through a free-market approach, while China achieved similar success using mobile-first infrastructure and a state-led strategy. Platforms like Alipay and WeChat Pay have adopted the renminbi as the primary asset to drive their financial services, especially for mobile users. As of June 2024, 969 million people were actively using mobile payments in China.[2]

Money itself is a form of technology that must evolve alongside economic advancement. While the dollar and renminbi provided the foundation, their true potential emerged through technological transformation–from basic electronic transfers to sophisticated digital payment networks. This evolution demonstrates a crucial pattern: as economies grow more complex, they demand more capable forms of money. The rise of blockchain technology and digital currencies represents the next frontier in this progression, promising not just to enhance existing monetary systems but to enable entirely new forms of economic activity and value exchange that were previously impossible. Much like how digital payments revolutionized traditional currencies, blockchain infrastructure such as stablecoins has the potential to unlock unprecedented levels of financial innovation and economic growth.

The Advent of Stablecoins Solving Modern Financial Problems

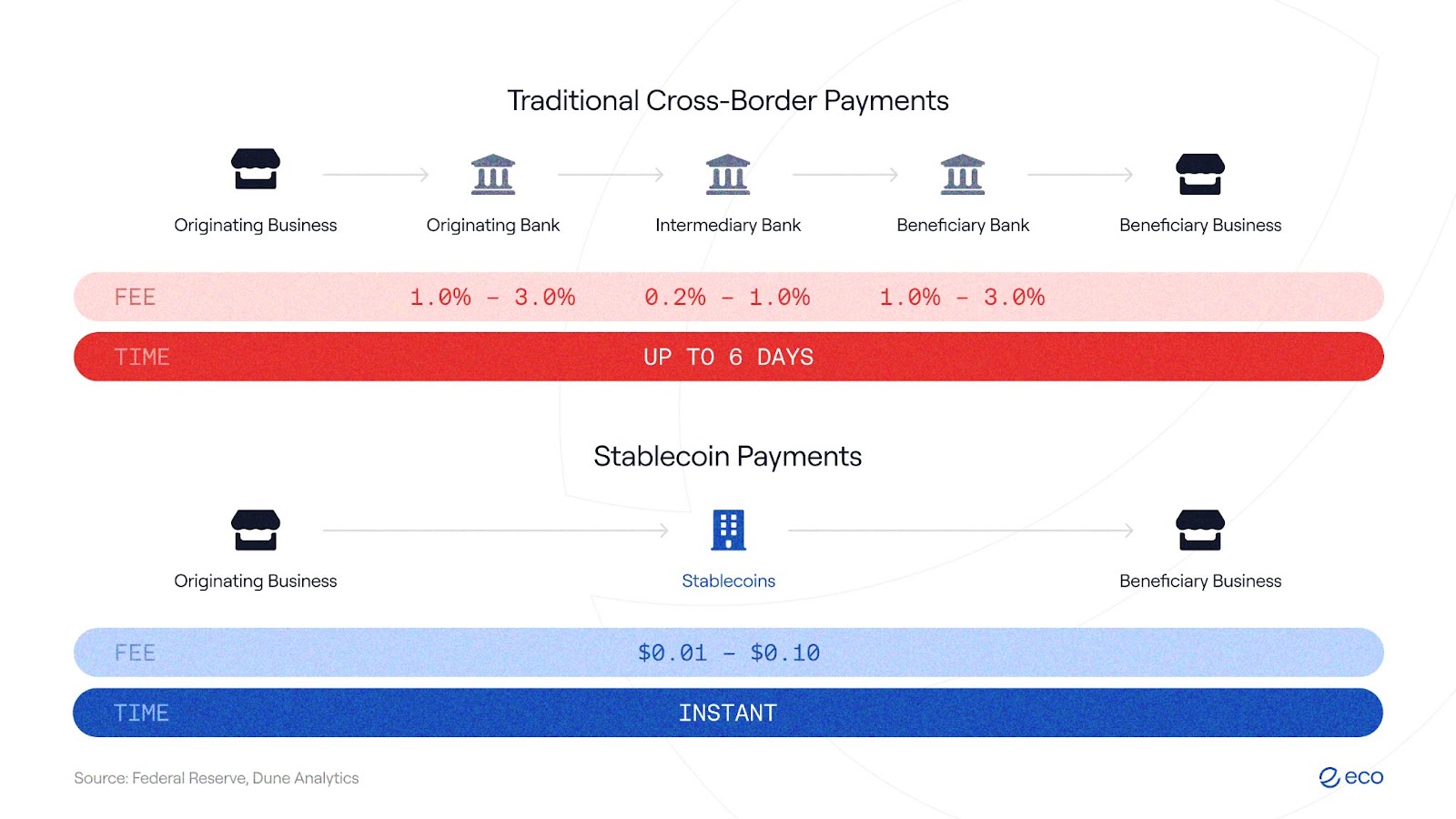

Despite many improvements in infrastructure for currencies, the world’s money systems still have room for significant improvement—SWIFT and CIPS still require at least a day to settle transactions; financial intermediaries that help facilitate payments charge high fees that ultimately extract value from the payer and payee; and apps like Venmo and Alipay do not provide simple means to transfer funds to and from other apps. What was realized about a decade ago is that a whole new asset class was needed to address these legacy issues.

Stablecoins eliminate the need for multiple intermediaries to facilitate complex transactions like cross-border payments and inter-app transfers. Stablecoin transactions can settle in seconds, and the number of intermediaries needed to facilitate transactions is significantly reduced. When a stablecoin transfer is completed, the sender can rest assured that only negligible fees are deducted, as transfers settled using blockchain can be as low as a fraction of a cent. The sender can also have confidence that the payment will be received and that no third party will cause issues with the transfer–simply examine the blockchain transaction history.

Given those benefits, stablecoins can supercharge many traditional assets, like sovereign currencies and commodities, into hyper-efficient, more resilient assets and mediums of exchange. Governments themselves are taking notice. Today, 134 countries and currency unions, representing 98% of global GDP, are exploring the issuance of some version of blockchain-based digital currencies. This number was only 35 in May 2020.[3] Historical leaders of currency innovation, like China, launched pilot programs around the digital renminbi. Instead of issuing central bank currencies wholesale to banks and other financial institutions, the central bank can now directly issue its currency to the people.

If stablecoins already show significant advantages over legacy systems, then why are stablecoins not yet the dominant asset for all payments? Market data may suggest that ease of use may be at the center of this problem.

The Critical Role of New Stablecoin Infrastructure for Widespread Adoption

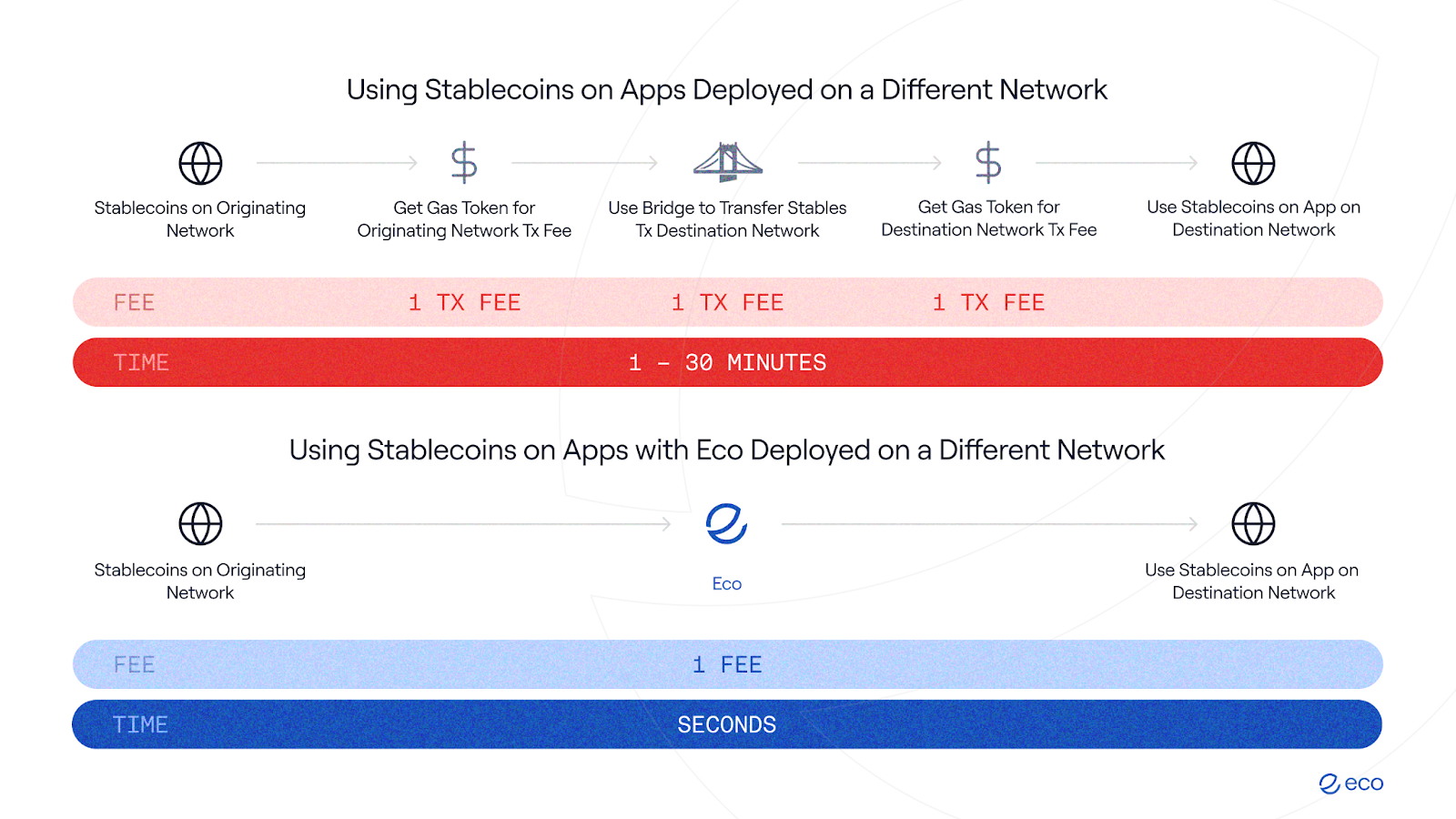

Despite their potential, stablecoins face one critical hurdle: usage complexity. The current user experience can be daunting for newcomers, who must often navigate a technical maze of new wallet setups and figure out how to fund that wallet before making their first transaction. Additionally, users must understand how to use onchain applications once they set up and fund their wallets. Similar to the setup process, successfully using onchain apps typically require knowledge of network compatibility, token compatibility, funding protocol gas fees, and more.

According to Crypto.com, there were 617 million crypto owners worldwide in June 2024. Artemis Terminal's data from December 2024 showed that stablecoin usage peaked at 2.9 million daily active addresses. Using a conservative estimate where each active address represents one user suggests that only 0.5% of global crypto holders use stablecoins onchain daily.

Just as new infrastructure like digital banking and mobile payments helped the U.S. dollar and Chinese renminbi grow, stablecoins represent a similar opportunity to scale currencies and economic activity more than ever before. But first, we must ensure that stablecoin infrastructure makes the onchain user experience as easy as possible, streamlining challenges like onchain setup and app usage and simplifying the transaction experience into a single click.

The Eco Protocol is the solution for any onchain app looking to make it as easy as possible for its users to get onchain (or cross-chain) and use stablecoins, regardless of network or the specific stablecoin asset. By unifying both Routes and Accounts for the Eco V1 launch, anyone interested in using apps with Eco integrated will no longer have to worry about the network or asset type. Instead, using stablecoins within these apps simplifies the process to just one action. The process is now as simple as keeping stablecoins and spending them like you would at any online store.

As solutions like the Eco Protocol emerge to break down technical barriers and streamline the user experience, stablecoins can finally realize their full potential. The future of money isn't just about creating better currencies—it's about democratizing access to efficient, borderless financial systems that truly work for everyone.

About Eco

Eco is the stablecoin network that makes money programmable across every major blockchain. Developers use Eco to power stablecoin flows that require seamless user experience and best-in-class execution — cross-chain transfers and swaps, programmable account logic, fast deposits, and more complex automations. Money simply moves smarter with Eco.

Website | Eco Docs | Twitter | LinkedIn | YouTube

About Eco Inc.

Eco Inc. builds technology that powers smarter, real-time money movement using stablecoins. We expect better from our money. That’s what drives us every day.